Category: Business

TMB

New CME Tracking Requirement

AN IMPORTANT UPDATE REGARDING YOUR LICENSE RENEWAL REQUIREMENTS

Due to recent legislation enacted by the Texas Legislature, all health care practitioners in Texas will be required to have their continuing education compliance verified through a CE tracking system prior to license renewal. This requirement is mandated by state law.

To meet this requirement, the Texas Medical Board (TMB) has partnered with CE Broker as the official CE tracking platform. ALL TMB licensees should, at a minimum, establish a free, basic account with CE Broker.

Beginning September 1, 2026, licensees renewing their license must:

- Have an active CE Broker account (basic accounts are free)

- Ensure all completed continuing education is reported in CE Broke

If the Texas Medical Board cannot verify CE compliance through CE Broker, you will not be able to complete your license renewal.

Upcoming Informational Webinar

To support licensees through this transition, TMB—along with CE Broker—will be hosting a series of informational webinars providing a practical, step-by-step tutorial on using CE Broker to track, manage, and report CME, supporting audit readiness and ongoing compliance.

Audience: Physicians

Date: Wednesday, May 13, 2026

Time: 12:00–1:00 PM CT

Registration is limited to 1,000 participants so please sign up as soon as possible to secure your spot. Registration will remain open until all spots are filled.

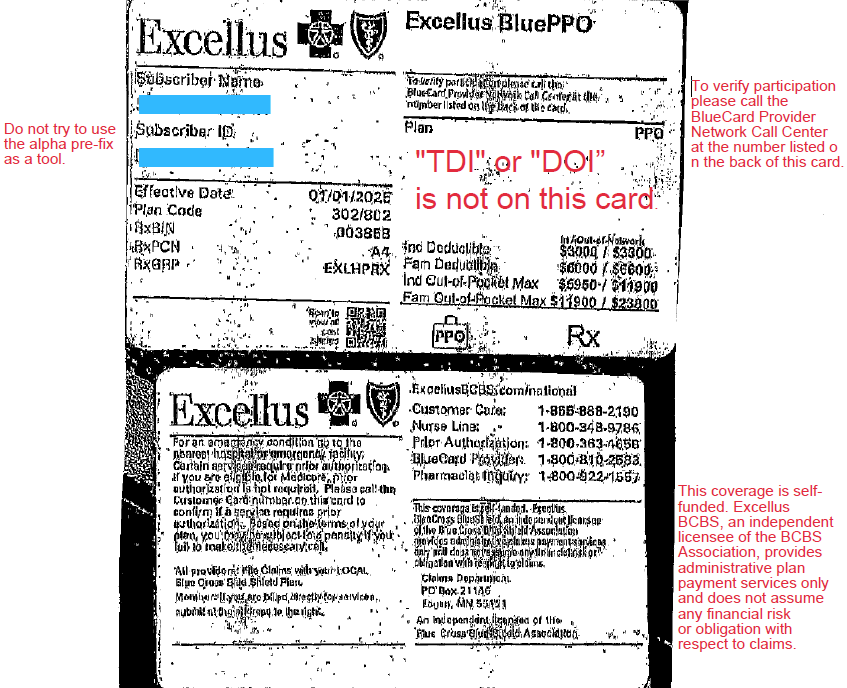

ERISA or maybe TPA?

Let’s play pretend:

Some one gives you this card and wants to make an appointment.

They seem to want an answer right now.

You know your physician takes Blue Choice, but have never seen this card before. How would you know?

Look at the front of the card. Blue Cross is written all over it. BCBS must be the insurer? STOP!

Do you see any insurance regulation language? Is “TDI” or “DOI” on this card?

NO. This is your 1st clue. The employer may be the insurer.

Scan the front of the card intently. Are there any other clues. Look for what you know, not what you don’t know.

If not flip it over. What do you see? READ ALL THE TINY WRITING.

On this card: phone numbers, addresses, where to file, prior auth info. But what else?

“This coverage is self-funded Excellus BlueCross BlueShield, and independent licensee of the BlueCross BlueShield Association provides administrative claims payment services only and does not assume any financial risk or obligation with respect to claims.”

What does that mean:

- The employer is the insurer (self-funded plan)

- Excellus BCBS is acting as a Third-Party Administrator (TPA)

Is this a Lease Network?

Very likely — yes.

On the front of the card it says:

“To verify participation, please call the BlueCard Provider Network.”

That suggests:

- The plan is using the BlueCard network

- Excellus is providing network access + claims processing. The employer is leasing the BCBS network

That’s what we commonly call a lease network arrangement.

But — this is important — don’t assume, Verify

Why you may still get a “Yes” when you call

When you call provider services:

- The rep may simply see “In Network”

- They may not understand lease networks

- They may not understand the difference between:

- Payor

- TPA

- Repricer

- Network administrator

So we need to ask better questions.

Instead of just asking “Is Dr. Smith in network?”

Tell the representative you would like to check network participation.

Ask:

- Is this plan self-funded? (if it is self-funded it is not a lease network)

- Is Excellus the payor, or the administrator?

- Is this a leased network?

- Who bears the financial risk?

- Is Excellus repricing the claims?

- What network applies to this patient?

And always get:

✔ Representative name

✔ Date/time

✔ Call reference number

If the claim denies, that reference number becomes your leverage.

Why this matters

In lease network plans:

- The employer controls the benefits.

- The employer may carve out services.

- The employer may override network rules.

- The plan can be patient-specific.

Basically they can make up their own rules.

In practical terms — They have more flexibility than a fully insured DOI-regulated plan.

Protect Yourself when speaking to the patient.

Never speak in absolutes.

Use language like:

- “It looks like this is a self-funded plan…”

- “Based on the card wording…”

- “According to the representative I spoke with…”

- “At the time of verification…”

Never say:

- “Yes, you are definitely covered.”

- “This will pay.”

- “You are in network.”

UHC Provider Webinar February 26, 2026

- Learn about digital tools to simplify workflow

- Explore UHC plans

- Hear Policy Updates

CMS-1500 vs Electronic Claims (837P)

What is a HCFA anyway?

POET understands, not everyone is a biller, and we might be throwing out alphabet soup to some office personal.

What is a CMS-1500 (HCFA) Form?

The CMS-1500, often still called a HCFA, is the standard paper form used to bill insurance companies for professional services provided by physicians and other healthcare providers.

It tells the insurance company:

Who the patient is

Who the provider is

What services were performed

When the services occurred

Why they were medically necessary

How much is being charged

What is Used When Claims Are Filed Electronically?

When an office files claims electronically, the equivalent of the CMS-1500 form is an: ANSI 837P Claim

837 = electronic claim format

P = Professional services

The 837P contains the same information as a CMS-1500, just in a computer-readable format instead of paper.

Why Staff May Not “See” an 837P

The billing software creates it automatically

It is sent through a clearinghouse

Insurance companies process it behind the scenes

Most staff interact with screens and reports, not the actual electronic file.

If You Need to See a “Paper Copy” of an 837P

An 837P does not have a true paper form. However, billing systems can produce a claim print image or CMS-1500-style report that shows the same data contained in the electronic claim.

This is often called:

Claim print image

CMS-1500 claim view

Electronic claim summary

These reports are used for: (Why POET would request it)

Reviewing what was sent

Troubleshooting rejections or denials

Sharing claim details with non-billing staff

Important: This is a readable representation of the 837P data — not the actual electronic file.

To see the raw 837P file itself, billing staff would need to export or view it through the billing system or clearinghouse.

Disclaimer: The information provided in this blog is for general educational purposes only. While Ink strives to explain insurance concepts accurately and clearly, payer rules, contracts, and policies can vary widely by plan, state, and provider agreement—and they change frequently.

This content should not be interpreted as definitive guidance or a substitute for reviewing payer manuals, contracts, or official communications. Physician offices are encouraged to conduct their own research and verify requirements directly with the applicable insurance carriers before making operational or billing decisions.

NEW BCBSTX fee schedule coming

ATTENTION PROVIDERS

BCBSTX has notified POET that a NEW Fee Schedule for Blue Choice and Blue Essentials will be effective May 1, 2026.

Once POET receives the new fee schedule and completes its review, OPT-IN / OPT-OUT packets will be sent to physician offices for participation decisions.

Please watch for additional communication once the review process is complete

What is an EPO

In health insurance, an EPO is an Exclusive Provider Organization plan.

Here’s what that means in practical terms:

What an EPO plan is

You must use doctors, hospitals, and facilities in the plan’s network

👉 Except for true emergenciesYou do not need a referral to see a specialist

Care received outside the network is not covered at all (again, except emergencies)

Pros of an EPO

Usually lower monthly premiums than PPO plans

No primary care referral requirement

Simpler than HMO plans

Cons of an EPO

No out-of-network coverage

Limited flexibility if you travel a lot or want a specific doctor who isn’t in-network

How EPO compares to other plans

EPO vs PPO: PPO allows out-of-network care (at higher cost); EPO does not

EPO vs HMO: HMO usually requires referrals; EPO does not

Disclaimer: The information provided in this blog is for general educational purposes only. While Ink strives to explain insurance concepts accurately and clearly, payer rules, contracts, and policies can vary widely by plan, state, and provider agreement—and they change frequently.

This content should not be interpreted as definitive guidance or a substitute for reviewing payer manuals, contracts, or official communications. Physician offices are encouraged to conduct their own research and verify requirements directly with the applicable insurance carriers before making operational or billing decisions.

Employer Group PPO/EPO Hybrid

Interpreting insurance cards has never been easy, but with the constant changes in today’s insurance landscape, it has become nearly impossible.

Every week seems to bring a new insurance company—or an established insurer that has acquired several others, rebranded, and rewritten the rules.

On top of that, there are hybrid plans like POS and EPO, along with discount cards, medical cost-sharing programs, limited-benefit plans, and the growing model of Direct Primary Care.

The one pictured below is an ultimate example!

It takes hybrid to a new level of complexity.

By mixing the rules of PPO and EPO in one plan.

Therefore, I, Sir Seymore, have taken my red pen in hand in an effort to make sense of it all.

Feel free to download this card for your records.

CLIA-Checks No Longer Accepted

Per CMS CLIA Communications Update: This is your last chance to go paperless before we eliminate paper fee coupons and CLIA Certificates on March 1, 2026. In addition, laboratories must pay their CLIA certification and survey fees online (checks will no longer be accepted). Failure to go paperless may result in billing or certification issues.

When you switch to paperless, your laboratory will get:

• Email notifications from CMS

• Electronic fee coupons*

• Electronic CLIA certificate – no more waiting for it to come in the mail*

*This does not apply to CLIA-exempt states or state licensure.

To switch, you must either:

• Email your State Agency

Tip: Include your laboratory name, laboratory director or owner’s name, CLIA number, director or designee’s signature to help your State Agency make the switch.

• Contact your Accreditation Organization (for accredited labs).

They can add or update email addresses for the laboratories they survey.

Reach out to your State Agency or Accreditation Organization for assistance. For more details, visit Clinical Laboratory Improvement Amendments (CLIA).

UHC December Monthly Overview

Key changes for our Medicare Advantage plan

- In 2026, most UnitedHealthcare Medicare Advantage health maintenance organization (HMO) and point of service (POS) plans are referral plans. You can check plan referral requirements online.

- Starting Jan. 1, 2026, most members enrolled in UnitedHealthcare Medicare Advantage HMO/POS plans will be required to obtain a referral from their primary care provider (PCP) before accessing certain specialist services in outpatient, office or home settings. Referrals must be submitted by the PCP to UnitedHealthcare prior to the specialist visit. This also applies when members of HMO/POS plans are traveling and accessing the National Network. Learn more in our 2026 Medicare Advantage Referral Requirements Guideopen_in_new.

- Effective Jan. 1, 2026, new or existing members of UnitedHealthcare SNPs, including Chronic Special Needs Plans (C-SNP) and Dual Special Needs Plans (D-SNP), need a qualifying chronic condition to access benefits that cover healthy food and/or utilities. Providers may be contacted by UnitedHealthcare to verify a member has at least one qualifying condition to receive benefits. See 2026 Medicare Advantage, CSNP & DSNP Plan Overview Courseopen_in_new for more information.

Recent Comments